Renewables Case Study: Double Loop Optimization

[1]:

import pyomo.environ as pyo

from pyomo.common.dependencies import check_min_version

import idaes

if not check_min_version(idaes, '2.0.0.a4'):

raise EnvironmentError("This notebook requires the 2.0.0.a4 pre-release of idaes-pse, which can be found here: https://github.com/dguittet/idaes-pse/tree/2.0.0.a4")

from dispatches_sample_data import rts_gmlc

from dispatches.models.renewables_case.wind_battery_double_loop import MultiPeriodWindBattery

from dispatches.models.renewables_case.double_loop_utils import *

for solver in ('xpress_direct', 'gurobi', 'cbc'):

if pyo.SolverFactory(solver).available(exception_flag=False):

milp_solver = solver

break

Creating the Co-simulation of the Wind and Battery IES within the Production Cost Model with Bidder and Tracker Models

In the Conceptual Design Optimization Example Notebook, the design of a Wind + Battery + Hydrogen integrated energy system was optimized using the RTS-GMLC outputs with a “price taker” assumption. Here, we take one of the possible results, a Wind + Battery IES with no Hydrogen, and evaluate its performance in an electricity market by co-simulating its bidding and operation decisions within the production cost model, Prescient, in a “double-loop” optimization.

This double-loop is performed by embedding the multiperiod Wind + Battery flowsheet model as a MultiPeriodWindBattery within a Bidder and a Tracker model, whose functions are to optimize the Day-ahead or Real-time energy market bids, and to optimize the operation of the IES to follow the cleared market’s dispatch, respectively. These functions are coordinated in order and with the correct data transfers with Prescient by a DoubleLoopCoordinator class. Prescient is then able to

evaluate the economic performance of the designed IES within the grid with market interactions and forecast uncertainty. The steps are as shown in this diagram:

In the Day-ahead loop, the Unit Commitment Problem is solved by forecasting loads and obtaining generator bids, and produces hourly schedules and LMPs. The Bidder will use forecasts and plant information to optimize the DA bid to Prescient.

In the Real-time loop, the Economic Dispatch Problem is solved using real-time loads and resources to produce updated generator dispatch points and commitments. The Bidder will use forecasts, DA dispatch and prices, and plant information to optimize the updated RT bid. Once the Real-time market is cleared, the Tracker controls the IES to implement the dispatch at lowest cost.

The market participants are paid on energy and/or reserve provided based on the two-settlement system:

where \(R\) is revenue, \(Q_{DA}\) is power sold to DA market at \(P_{DA}\) price, and \(Q_{RT}\) is power delivered to RT market at \(P_{RT}\) price.

First, we define the electricity grid for the double-loop simulation via options to Prescient: the directory to the RTS-GMLC source data, the time horizons for the UC and ED problems, the start date and length of the simulation, how much reserves should be procured, etc. The full-year PCM simulation was completed prior and the outputs were collected into a 309_WIND_1-SimulationOutputs.csv in order to provide “historical” LMPs and Wind resource capacity factors for the Conceptual Design

Optimization.

In this example, we will repeat the Prescient simulation with no reserves for a single week, where the Wind + Battery IES will replace the 309_WIND_1 Wind plant at the “Carter” bus.

[2]:

from prescient.simulator import Prescient

import os

start_date = "01-02-2020"

sim_days = 7

day_ahead_horizon = 48

real_time_horizon = 4

output_dir = Path(f"double_loop_results")

wind_bus = 309

wind_bus_name = "Carter"

wind_generator = f"{wind_bus}_WIND_1"

prescient_options = {

"data_path": rts_gmlc.source_data_path,

"input_format": "rts-gmlc",

"simulate_out_of_sample": True,

"run_sced_with_persistent_forecast_errors": True,

"output_directory": output_dir,

"start_date": start_date,

"num_days": sim_days,

"sced_horizon": real_time_horizon,

"ruc_horizon": day_ahead_horizon,

"compute_market_settlements": True,

"day_ahead_pricing": "LMP",

"ruc_mipgap": 0.05,

"symbolic_solver_labels": True,

"reserve_factor": 0,

"deterministic_ruc_solver": milp_solver,

"sced_solver": milp_solver,

"plugin": {

"doubleloop": {

"module": None, # to be added below

"bidding_generator": wind_generator,

}

}

}

# collect "historical" full-year wind forecast and first-day LMPs

prescient_outputs_df = pd.read_csv(Path(os.path.realpath("__file__")).parent / "data" / "309_WIND_1-SimulationOutputs.csv")

prescient_outputs_df.index = pd.to_datetime(prescient_outputs_df['Unnamed: 0'])

prescient_outputs_df = prescient_outputs_df[prescient_outputs_df.index >= pd.Timestamp(f'{start_date} 00:00:00')]

gen_capacity_factor = prescient_outputs_df[f"{wind_generator}-RTCF"].values.tolist()

historical_da_prices = {

wind_bus_name: prescient_outputs_df[f"LMP DA"].values[0:24].tolist()

}

historical_rt_prices = {

wind_bus_name: prescient_outputs_df[f"LMP"].values[0:24].tolist()

}

Interactive Python mode detected; using default matplotlib backend for plotting.

[3]:

from matplotlib.ticker import MultipleLocator

import matplotlib.pyplot as plt

plt.rcParams.update({'font.size': 16, 'axes.titlesize': 16, 'axes.labelsize': 14})

def format_plt(fig, ax, titles, suptitle=None, mod_ticks=True, y_labels=None):

if not y_labels:

y_labels = ["Power [MW]"] * len(ax)

for i in range(len(ax)):

if mod_ticks:

ax[i].xaxis.set_minor_locator(MultipleLocator(4))

ax[i].xaxis.set_major_locator(MultipleLocator(24))

ax[i].tick_params(axis='both', which='major', labelsize="small")

ax[i].tick_params(axis='both', which='minor', labelsize="small")

ax[i].legend()

ax[i].set_ylabel(y_labels[i])

ax[i].set_xlabel("Time [hr]")

ax[i].set_title(titles[i])

fig.autofmt_xdate(rotation=45)

if suptitle:

fig.suptitle(suptitle)

fig.tight_layout()

time_index = prescient_outputs_df[prescient_outputs_df.index <= '2020-01-08 23:00:00'].index

orig_outputs_df = prescient_outputs_df[prescient_outputs_df.index.isin(time_index)].copy()

orig_outputs_df['Penalized DA Underdelivered [MW]'] = (orig_outputs_df['Output DA'] - orig_outputs_df['Output']) * (orig_outputs_df['LMP'] > orig_outputs_df['LMP DA'])

orig_outputs_df.loc[:, 'Penalized DA Underdelivered [MW]'].clip(lower=0, inplace=True)

orig_outputs_df['Curtailment'] *= -1

fig, ax = plt.subplots(2, 1, figsize=(24, 10), sharex=True)

ax[0].plot(orig_outputs_df['Output DA'].values, drawstyle="steps-mid", label='DA Dispatch [MW]', color='grey')

ax[0].plot(orig_outputs_df['Output'].values, drawstyle="steps-mid", label='RT Dispatch [MW]', color='k')

cols = ['Output', 'Penalized DA Underdelivered [MW]']

orig_outputs_df[cols].plot(kind='bar', width=1, stacked=True, ax=ax[0], color=['b', 'r'])

orig_outputs_df['Curtailment'].plot(kind='bar', width=1, stacked=True, ax=ax[1])

format_plt(fig, ax, titles=["Wind Output vs Dispatch", "Wind Curtailment"], suptitle="Original RTS-GMLC Simulation")

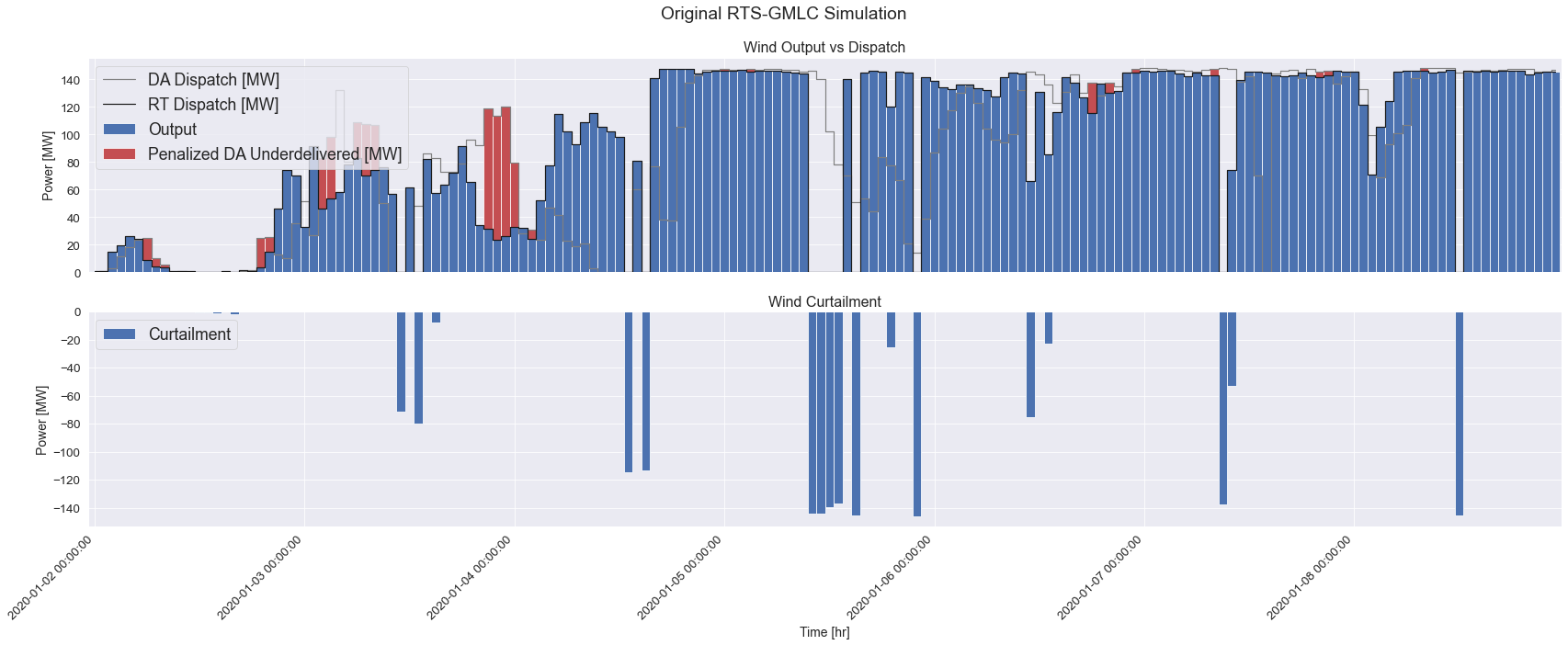

The above plot shows the wind plant’s DA Dispatch, RT Dispatch, Wind Power Output, Penalized DA Underdelivered, and Wind Curtailment in MW for the first week. The DA and RT Dispatch profiles are from the final solution of Prescient’s staggered and forward-rolling UC and ED problems, and are based on the day-ahead and real-time wind forecast, respectively.

The Wind Power Output is the real-time wind production of the wind plant, and matches the RT Dispatch exactly. However, since there was uncertainty of the RT wind resource during the DA bid, the DA Dispatch is different. According to the two-settlement system revenue equation above, the wind plant will be charged the RT LMP for the difference between the promised DA Dispatch and the delivered RT power. The Penalized DA Underdelivered profile show the power that was underdelivered

when RT LMPs were higher than DA LMPs and resulted in some negative revenue for the plant.

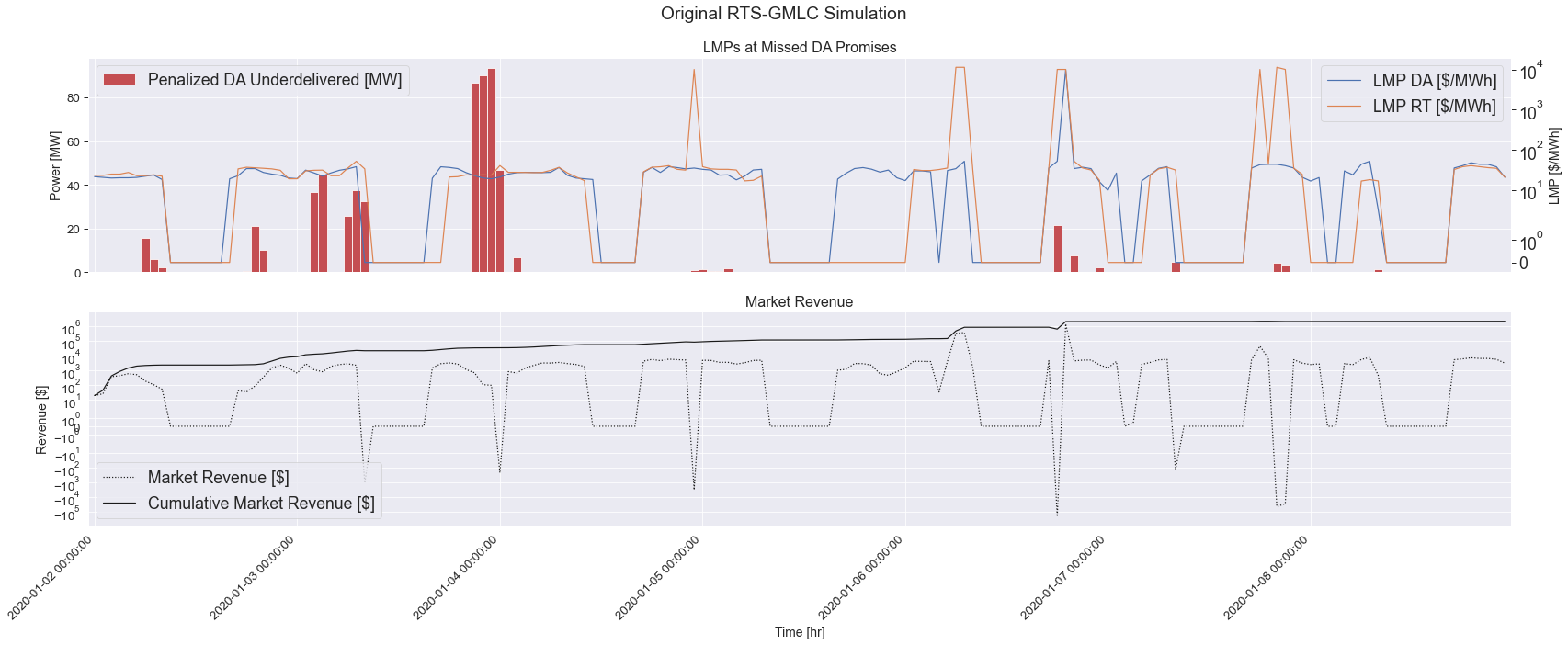

The second plot below shows the Hourly and Cumulative revenue of the wind plant.

[4]:

fig, ax = plt.subplots(2, 1, figsize=(24, 10), sharex=True)

orig_outputs_df['Penalized DA Underdelivered [MW]'].plot(ax=ax[0], color='r', kind='bar', width=1)

ax0 = ax[0].twinx()

ax0.set_yscale('symlog')

ax0.plot(orig_outputs_df['LMP DA'].values, label="LMP DA [$/MWh]")

ax0.plot(orig_outputs_df['LMP'].values, label='LMP RT [$/MWh]')

ax0.legend(loc='upper right')

ax0.grid(None)

ax0.set_ylabel("LMP [$/MWh]")

ax[1].set_yscale('symlog')

ax[1].plot(orig_outputs_df['Unit Market Revenue'].values, color='k', linestyle=':', label="Market Revenue [$]")

ax[1].plot(orig_outputs_df['Unit Market Revenue'].cumsum().values, color='k', label="Cumulative Market Revenue [$]")

format_plt(fig, ax, y_labels=['Power [MW]', 'Revenue [$]'], titles=["LMPs at Missed DA Promises", "Market Revenue"], suptitle="Original RTS-GMLC Simulation")

ax[0].legend(loc='upper left')

[4]:

<matplotlib.legend.Legend at 0x7fd7992c13d0>

Creating the IES Generator within the RTS-GMLC

First, the location, type, capacity, and other parameters of the IES needs to be defined in order to situate the generator within the electricity market. In this example, the IES’ bid will be represented as that of a thermal generator, with parameters such as min power, max power, ramping constraints, startup and shutdown capacity, even though the IES will not need them all. The wind resource at the chosen location, at the “Carter” bus, is read from the RTS-GMLC Source Data.

The information is passed to the MultiPeriodWindBattery class, which enables the Bidder and Tracker to construct a Wind + Battery multiperiod model within its bidding and tracking optimization problems via populate_model, and to update the state of the Wind + Battery IES as the double-loop steps forward in time via update_model.

[5]:

from idaes.apps.grid_integration.model_data import ThermalGeneratorModelData

p_min = 0

wind_pmax = 147.6

battery_pmax = 25

battery_emax = battery_pmax * 4

# for descriptions on what each parameter means, see `help(ThermalGeneratorModelData)`

thermal_generator_params = {

"gen_name": wind_generator,

"bus": wind_bus_name,

"p_min": p_min,

"p_max": wind_pmax,

"min_down_time": 0,

"min_up_time": 0,

"ramp_up_60min": wind_pmax + battery_pmax,

"ramp_down_60min": wind_pmax + battery_pmax,

"shutdown_capacity": wind_pmax + battery_pmax,

"startup_capacity": 0,

"initial_status": 1,

"initial_p_output": 0,

"production_cost_bid_pairs": [(p_min, 0), (wind_pmax, 0)],

"startup_cost_pairs": [(0, 0)],

"fixed_commitment": None,

}

model_data = ThermalGeneratorModelData(**thermal_generator_params)

mp_wind_battery_bid = MultiPeriodWindBattery(

model_data=model_data,

wind_capacity_factors=gen_capacity_factor,

wind_pmax_mw=wind_pmax,

battery_pmax_mw=battery_pmax,

battery_energy_capacity_mwh=battery_emax,

)

Creating the Forecaster, Tracker, and Bidder for the DoupleLoopCoordinator

The Bidder requires a forecast of the DA and RT prices in order to plan out its energy bid: at what time to sell how much energy and at what price, given the anticipated wind resource and the evolution of the battery state-of-charge. In contrast to the price-taker assumption in the Conceptual Design phase where the Wind + Battery IES took the historical LMPs for however much energy it sold, here, the Bidder does not know what the final LMP will be, nor that its bid for energy at a

certain marginal cost will be accepted by the market.

The Backcaster class stores historical DA and RT LMPs in order to generate forecast scenarios. The first day of simulated DA and RT LMPs initializes the Backcaster, which continues to collect resolved LMPs as the simulation steps forward in time.

Within the DoubleLoopCoordinator, there are two Tracker objects, the first tracker follows the real-time market signals whereas the second projection_tracker projects the latest real-time dispatch onto the next day-ahead bidding problem.

[6]:

from idaes.apps.grid_integration.forecaster import Backcaster

from idaes.apps.grid_integration import Tracker, DoubleLoopCoordinator, Bidder

# Backcaster

help(Backcaster)

backcaster = Backcaster(historical_da_prices, historical_rt_prices)

Help on class Backcaster in module idaes.apps.grid_integration.forecaster:

class Backcaster(AbstractPrescientPriceForecaster)

| Backcaster(historical_da_prices, historical_rt_prices, max_historical_days=10)

|

| Generate price forecasts by directly using historical prices.

|

| Method resolution order:

| Backcaster

| AbstractPrescientPriceForecaster

| AbstractPriceForecaster

| abc.ABC

| builtins.object

|

| Methods defined here:

|

| __init__(self, historical_da_prices, historical_rt_prices, max_historical_days=10)

| Initialize the Backcaster.

|

| Arguments:

| historical_da_prices: dictionary of list for historical hourly day-ahead prices

|

| historical_rt_prices: dictionary of list for historical hourly real-time prices

|

| max_historical_days: maximum number of days of price data to store on the instance

|

| Returns:

| None

|

| fetch_day_ahead_stats_from_prescient(self, uc_date, uc_hour, day_ahead_result)

| This method fetches the hourly day-ahead prices from Prescient and store

| them on the price forecaster, once they are published. When the stored historical

| data size has exceeded the specified upper bound, drop the oldest data.

|

| Arguments:

| ruc_date: the date of the day-ahead market we bid into.

|

| ruc_hour: the hour the RUC is being solved in the day before.

|

| day_ahead_result: a Prescient RucPlan object.

|

| Returns:

| None

|

| fetch_hourly_stats_from_prescient(self, prescient_hourly_stats)

| This method fetches the hourly real-time prices from Prescient and store

| them on the price forecaster, once they are published. When the stored historical

| data size has exceeded the specified upper bound, drop the oldest data.

|

| Arguments:

| prescient_hourly_stats: Prescient HourlyStats object.

|

| Returns:

| None

|

| forecast_day_ahead_and_real_time_prices(self, date, hour, bus, horizon, n_samples)

| Forecast both day-ahead and real-time market prices.

|

| Arguments:

| date: intended date of the forecasts

|

| hour: intended hour of the forecasts

|

| bus: intended bus of the forecasts

|

| horizon: number of the time periods of the forecasts

|

| n_samples: number of the samples

|

| Returns:

| dict: day-ahead price forecasts

|

| dict: real-time price forecasts

|

| forecast_day_ahead_prices(self, date, hour, bus, horizon, n_samples)

| Forecast day-ahead market prices.

|

| Arguments:

| date: intended date of the forecasts

|

| hour: intended hour of the forecasts

|

| bus: intended bus of the forecasts

|

| horizon: number of the time periods of the forecasts

|

| n_samples: number of the samples

|

| Returns:

| dict: day-ahead price forecasts

|

| forecast_real_time_prices(self, date, hour, bus, horizon, n_samples)

| Forecast real-time market prices.

|

| Arguments:

| date: intended date of the forecasts

|

| hour: intended hour of the forecasts

|

| bus: intended bus of the forecasts

|

| horizon: number of the time periods of the forecasts

|

| n_samples: number of the samples

|

| Returns:

| dict: real-time price forecasts

|

| ----------------------------------------------------------------------

| Data descriptors defined here:

|

| historical_da_prices

| Property getter for historical_da_prices.

|

| Returns:

| dict: saved historical day-ahead prices

|

| historical_rt_prices

| Property getter for historical_rt_prices.

|

| Returns:

| dict: saved historical real-time prices

|

| max_historical_days

| Property getter for max_historical_days.

|

| Returns:

| int: max historical days

|

| ----------------------------------------------------------------------

| Data and other attributes defined here:

|

| __abstractmethods__ = frozenset()

|

| ----------------------------------------------------------------------

| Data descriptors inherited from AbstractPriceForecaster:

|

| __dict__

| dictionary for instance variables (if defined)

|

| __weakref__

| list of weak references to the object (if defined)

[7]:

n_price_scenario = 3

solver = pyo.SolverFactory(milp_solver)

# Bidder

help(Bidder)

bidder_mp_wind_battery = MultiPeriodWindBattery(

model_data=model_data,

wind_capacity_factors=gen_capacity_factor,

wind_pmax_mw=wind_pmax,

battery_pmax_mw=battery_pmax,

battery_energy_capacity_mwh=battery_emax,

)

bidder_object = Bidder(

bidding_model_object=bidder_mp_wind_battery,

day_ahead_horizon=day_ahead_horizon,

real_time_horizon=real_time_horizon,

n_scenario=n_price_scenario,

solver=solver,

forecaster=backcaster,

)

Help on class Bidder in module idaes.apps.grid_integration.bidder:

class Bidder(StochasticProgramBidder)

| Bidder(bidding_model_object, day_ahead_horizon, real_time_horizon, n_scenario, solver, forecaster)

|

| Wrap a model object to bid into the market using stochastic programming.

|

| Method resolution order:

| Bidder

| StochasticProgramBidder

| AbstractBidder

| abc.ABC

| builtins.object

|

| Methods defined here:

|

| __init__(self, bidding_model_object, day_ahead_horizon, real_time_horizon, n_scenario, solver, forecaster)

| Initializes the bidder object.

|

| Arguments:

| bidding_model_object: the model object for bidding

|

| day_ahead_horizon: number of time periods in the day-ahead bidding problem

|

| real_time_horizon: number of time periods in the real-time bidding problem

|

| n_scenario: number of uncertain LMP scenarios

|

| solver: a Pyomo mathematical programming solver object

|

| forecaster: an initialized LMP forecaster object

|

| Returns:

| None

|

| ----------------------------------------------------------------------

| Data and other attributes defined here:

|

| __abstractmethods__ = frozenset()

|

| ----------------------------------------------------------------------

| Methods inherited from StochasticProgramBidder:

|

| compute_day_ahead_bids(self, date, hour=0)

| Solve the model to bid into the day-ahead market. After solving, record

| the bids from the solve.

|

| Arguments:

|

| date: current simulation date

|

| hour: current simulation hour

|

| Returns:

| dict: the obtained bids

|

| compute_real_time_bids(self, date, hour, realized_day_ahead_prices, realized_day_ahead_dispatches)

| Solve the model to bid into the real-time market. After solving, record

| the bids from the solve.

|

| Arguments:

|

| date: current simulation date

|

| hour: current simulation hour

|

| Returns:

| dict: the obtained bids

|

| formulate_DA_bidding_problem(self)

| Set up the day-ahead stochastic programming bidding problems.

|

| Returns:

| pyomo.core.base.PyomoModel.ConcreteModel: base bidding model

|

| formulate_RT_bidding_problem(self)

| Set up the real-time stochastic programming bidding problems.

|

| Returns:

| pyomo.core.base.PyomoModel.ConcreteModel: base bidding model

|

| record_bids(self, bids, model, date, hour, market)

| This function records the bids and the details in the underlying bidding model.

|

| Arguments:

| bids: the obtained bids for this date.

|

| model: bidding model

|

| date: the date we bid into

|

| hour: the hour we bid into

|

| Returns:

| None

|

| update_day_ahead_model(self, **kwargs)

| This method updates the parameters in the day-ahead model based on the implemented profiles.

|

| Arguments:

| kwargs: the newly implemented stats. {stat_name: [...]}

|

| Returns:

| None

|

| update_real_time_model(self, **kwargs)

| This method updates the parameters in the real-time model based on the implemented profiles.

|

| Arguments:

| kwargs: the newly implemented stats. {stat_name: [...]}

|

| Returns:

| None

|

| write_results(self, path)

| This methods writes the saved operation stats into an csv file.

|

| Arguments:

| path: the path to write the results.

|

| Return:

| None

|

| ----------------------------------------------------------------------

| Data descriptors inherited from StochasticProgramBidder:

|

| generator

|

| ----------------------------------------------------------------------

| Data descriptors inherited from AbstractBidder:

|

| __dict__

| dictionary for instance variables (if defined)

|

| __weakref__

| list of weak references to the object (if defined)

[8]:

tracking_horizon = 4

n_tracking_hour = 1

# Tracker

help(Tracker)

tracker_mp_wind_battery = MultiPeriodWindBattery(

model_data=model_data,

wind_capacity_factors=gen_capacity_factor,

wind_pmax_mw=wind_pmax,

battery_pmax_mw=battery_pmax,

battery_energy_capacity_mwh=battery_emax,

)

tracker_object = Tracker(

tracking_model_object=tracker_mp_wind_battery,

tracking_horizon=tracking_horizon,

n_tracking_hour=n_tracking_hour,

solver=solver,

)

# Projection Tracker

projection_mp_wind_battery = MultiPeriodWindBattery(

model_data=model_data,

wind_capacity_factors=gen_capacity_factor,

wind_pmax_mw=wind_pmax,

battery_pmax_mw=battery_pmax,

battery_energy_capacity_mwh=battery_emax,

)

projection_tracker_object = Tracker(

tracking_model_object=projection_mp_wind_battery,

tracking_horizon=tracking_horizon,

n_tracking_hour=n_tracking_hour,

solver=solver,

)

Help on class Tracker in module idaes.apps.grid_integration.tracker:

class Tracker(builtins.object)

| Tracker(tracking_model_object, tracking_horizon, n_tracking_hour, solver)

|

| Wrap a model object to track the market dispatch signals. This class interfaces

| with the DoubleLoopCoordinator.

|

| Methods defined here:

|

| __init__(self, tracking_model_object, tracking_horizon, n_tracking_hour, solver)

| Initializes the tracker object.

|

| Arguments:

| tracking_model_object: the model object for tracking

|

| tracking_horizon: number of time periods in the tracking problem

|

| n_tracking_hour: number of implemented hours after each solve

|

| solver: a Pyomo mathematical programming solver object

|

| Returns:

| None

|

| formulate_tracking_problem(self)

| Formulate the tracking optimization problem by adding necessary

| parameters, constraints, and objective function.

|

| Arguments:

| None

|

| Returns:

| None

|

| get_last_delivered_power(self)

| Returns the last delivered power output.

|

| Arguments:

| None

|

| Returns:

| None

|

| record_results(self, **kwargs)

| Record the operations stats for the model.

|

| Arguments:

| kwargs: key word arguments that can be passed into tracking model object's record result function.

|

| Returns:

| None

|

| track_market_dispatch(self, market_dispatch, date, hour)

| Solve the model to track the market dispatch signals. After solving,

| record the results from the solve and update the model.

|

| Arguments:

| market_dispatch: a list that contains the market dispatch signals

|

| date: current simulation date

|

| hour: current simulation hour

|

| Returns:

| None

|

| update_model(self, **profiles)

| This method updates the parameters in the model based on the implemented profiles.

|

| Arguments:

| profiles: the newly implemented stats. {stat_name: [...]}

|

| Returns:

| None

|

| write_results(self, path)

| This methods writes the saved operation stats into an csv file.

|

| Arguments:

| path: the path to write the results.

|

| Return:

| None

|

| ----------------------------------------------------------------------

| Data descriptors defined here:

|

| __dict__

| dictionary for instance variables (if defined)

|

| __weakref__

| list of weak references to the object (if defined)

[9]:

# Compose into Coordinator

help(DoubleLoopCoordinator)

coordinator = DoubleLoopCoordinator(

bidder=bidder_object,

tracker=tracker_object,

projection_tracker=projection_tracker_object,

)

Help on class DoubleLoopCoordinator in module idaes.apps.grid_integration.coordinator:

class DoubleLoopCoordinator(builtins.object)

| DoubleLoopCoordinator(bidder, tracker, projection_tracker)

|

| Coordinate Prescient, tracker and bidder.

|

| Methods defined here:

|

| __init__(self, bidder, tracker, projection_tracker)

| Initializes the DoubleLoopCoordinator object and registers functionalities

| in Prescient's plugin system.

|

| Arguments:

| bidder: an initialized bidder object

|

| tracker: an initialized tracker object

|

| projection_tracker: an initialized tracker object, this object is

| mimicking the behaviror of the projection SCED in

| Prescient and to projecting the system states

| and updating bidder model.

|

| Returns:

| None

|

| activate_pending_DA_data(self, options, simulator)

| This function puts the day-ahead data computed in the day before into effect,

| i.e. the data for the next day become the data for the current day.

|

| Arguments:

| options: Prescient options from prescient.simulator.config.

|

| simulator: Prescient simulator.

|

| Returns:

| None

|

| assemble_project_tracking_signal(self, options, simulator, hour)

| This function assembles the signals for the tracking model to estimate the

| state of the bidding model at the beginning of next RUC.

|

| Arguments:

| options: Prescient options from prescient.simulator.config.

|

| simulator: Prescient simulator.

|

| hour: the simulation hour.

|

| Returns:

| market_signals: the market signals to be tracked.

|

| assemble_sced_tracking_market_signals(self, options, simulator, sced_instance, hour)

| This function assembles the signals for the tracking model.

|

| Arguments:

| options: Prescient options from prescient.simulator.config.

|

| simulator: Prescient simulator.

|

| sced_instance: Prescient SCED object

|

| hour: the simulation hour.

|

| Returns:

| market_signals: the market signals to be tracked.

|

| bid_into_DAM(self, options, simulator, ruc_instance, ruc_date, ruc_hour)

| This function uses the bidding objects to bid into the day-ahead market

| (DAM).

|

| Arguments:

| options: Prescient options from prescient.simulator.config.

|

| simulator: Prescient simulator.

|

| ruc_instance: Prescient RUC object.

|

| ruc_date: the date of the day-ahead market we bid into.

|

| ruc_hour: the hour the RUC is being solved in the day before.

|

| Returns:

| None

|

| bid_into_RTM(self, options, simulator, sced_instance)

| This function bids into the real-time market. At this moment I just copy the

| corresponding day-ahead bid here.

|

| Arguments:

| options: Prescient options from prescient.simulator.config.

|

| simulator: Prescient simulator.

|

| sced_instance: Prescient SCED object.

|

| Returns:

| None

|

| fetch_DA_dispatches(self, options, simulator, result, uc_date, uc_hour)

| This method fetches the day-ahead dispatches from unit commitment results,

| and save it as a coordinator attribute.

|

| Arguments:

| options: Prescient options from prescient.simulator.config.

|

| simulator: Prescient simulator.

|

| result: a Prescient RucPlan object.

|

| ruc_date: the date of the day-ahead market we bid into.

|

| ruc_hour: the hour the RUC is being solved in the day before.

|

| Returns:

| None

|

| fetch_DA_prices(self, options, simulator, result, uc_date, uc_hour)

| This method fetches the day-ahead market prices from unit commitment results,

| and save it as a coordinator attribute.

|

| Arguments:

| options: Prescient options from prescient.simulator.config.

|

| simulator: Prescient simulator.

|

| result: a Prescient RucPlan object.

|

| ruc_date: the date of the day-ahead market we bid into.

|

| ruc_hour: the hour the RUC is being solved in the day before.

|

| Returns:

| None

|

| get_configuration(self, key)

| Register customized commandline options.

|

| Arguments:

| key: plugin name

|

| Returns:

| config: Prescient config dict

|

| initialize_customized_results(self, options, simulator)

| This method is outdated.

|

| pass_static_params_to_DA(self, options, simulator, ruc_instance, ruc_date, ruc_hour)

| This method pass static generator parameters to RUC model in Prescient

| before it is solved.

|

| Arguments:

| options: Prescient options from prescient.simulator.config.

|

| simulator: Prescient simulator.

|

| ruc_instance: Prescient RUC object.

|

| ruc_date: the date of the day-ahead market we bid into.

|

| ruc_hour: the hour the RUC is being solved in the day before.

|

| Returns:

| None

|

| pass_static_params_to_RT(self, options, simulator, sced_instance)

| This method pass static generator parameters to SCED model in Prescient

| before it is solved.

|

| Arguments:

| options: Prescient options from prescient.simulator.config.

|

| simulator: Prescient simulator.

|

| sced_instance: Prescient SCED object.

|

| Returns:

| None

|

| project_tracking_trajectory(self, options, simulator, ruc_hour)

| This function projects the full power dispatch trajectory from the

| tracking model so we can use it to update the bidding model, i.e. advance

| the time for the bidding model.

|

| Arguments:

| options: Prescient options from prescient.simulator.config.

|

| simulator: Prescient simulator.

|

| ruc_hour: the hour RUC is being solved

|

| Returns:

| full_projected_trajectory: the full projected power dispatch trajectory.

|

| push_day_ahead_stats_to_forecaster(self, options, simulator, day_ahead_result, uc_date, uc_hour)

| This method pushes the day-ahead market to the price forecaster after the

| UC is solved.

|

| Arguments:

| options: Prescient options from prescient.simulator.config.

|

| simulator: Prescient simulator.

|

| day_ahead_result: a Prescient RucPlan object.

|

| ruc_date: the date of the day-ahead market we bid into.

|

| ruc_hour: the hour the RUC is being solved in the day before.

|

| Returns:

| None

|

| push_hourly_stats_to_forecaster(self, prescient_hourly_stats)

| This method pushes the hourly stats from Prescient to the price forecaster

| once the hourly stats are published.

|

| Arguments:

| prescient_hourly_stats: Prescient HourlyStats object.

|

| Returns:

| None

|

| register_plugins(self, context, options, plugin_config)

| Register functionalities in Prescient's plugin system.

|

| Arguments:

| context: Prescient plugin PluginRegistrationContext from prescient.plugins.plugin_registration

|

| options: Prescient options from prescient.simulator.config

|

| plugin_config: Prescient plugin config

|

| Returns:

| None

|

| track_sced_signal(self, options, simulator, sced_instance, lmp_sced)

| This methods uses the tracking object to track the current real-time market

| signals.

|

| Arguments:

| options: Prescient options from prescient.simulator.config.

|

| simulator: Prescient simulator.

|

| sced_instance: Prescient SCED object

|

| lmp_sced: Prescient SCED LMP object

|

| Returns:

| None

|

| update_observed_dispatch(self, options, simulator, ops_stats)

| This methods extract the actual power delivered by the tracking model and

| inform Prescient, so Prescient can use this data to calculate the settlement

| and etc.

|

| Arguments:

| options: Prescient options from prescient.simulator.config.

|

| simulator: Prescient simulator.

|

| ops_stats: Prescient operation statitstic object

|

| Returns:

| None

|

| write_plugin_results(self, options, simulator)

| After the simulation is completed, the plugins can write their own customized

| results. Each plugin will have to have a method named 'write_results'.

|

| Arguments:

| options: Prescient options from prescient.simulator.config.

|

| simulator: Prescient simulator.

|

| Returns:

| None

|

| ----------------------------------------------------------------------

| Data descriptors defined here:

|

| __dict__

| dictionary for instance variables (if defined)

|

| __weakref__

| list of weak references to the object (if defined)

Running the Double-Loop Plugin

The prescient_options are updated with the DoubleLoopCoordinator. The simulation results will be written to the output_dir folder.

[10]:

from types import ModuleType

import shutil

class PrescientPluginModule(ModuleType):

def __init__(self, get_configuration, register_plugins):

self.get_configuration = get_configuration

self.register_plugins = register_plugins

plugin_module = PrescientPluginModule(

get_configuration=coordinator.get_configuration,

register_plugins=coordinator.register_plugins,

)

prescient_options['plugin']['doubleloop']['module'] = plugin_module

if output_dir.exists():

shutil.rmtree(output_dir)

Prescient().simulate(**prescient_options)

[11]:

pd.set_option('display.max_columns', None)

pd.set_option('display.max_rows', None)

plt.style.use('seaborn')

df = double_loop_outputs_for_gen(output_dir, rts_gmlc.source_data_path)

prescient_df = df[df['Model'] == "Prescient"].copy()

da_bidder_df = df[df['Model'] == "DA Bidder"].copy()

rt_bidder_df = df[df['Model'] == "RT Bidder"].copy()

tracker_df = df[df['Model'] == "Tracker"].copy()

tracker_df.loc[:, 'Wind Curtailment [MW]'] = tracker_df['Wind Curtailment [MW]'] * -1

time_index = prescient_df.index

time_slice = slice(0, len(time_index))

da_bid_powers = [i for i in da_bidder_df.columns if 'DA Power' in i]

rt_bid_powers = [i for i in da_bidder_df.columns if 'RT Power' in i]

Analyzing the Wind + Battery IES Performance: Bidder

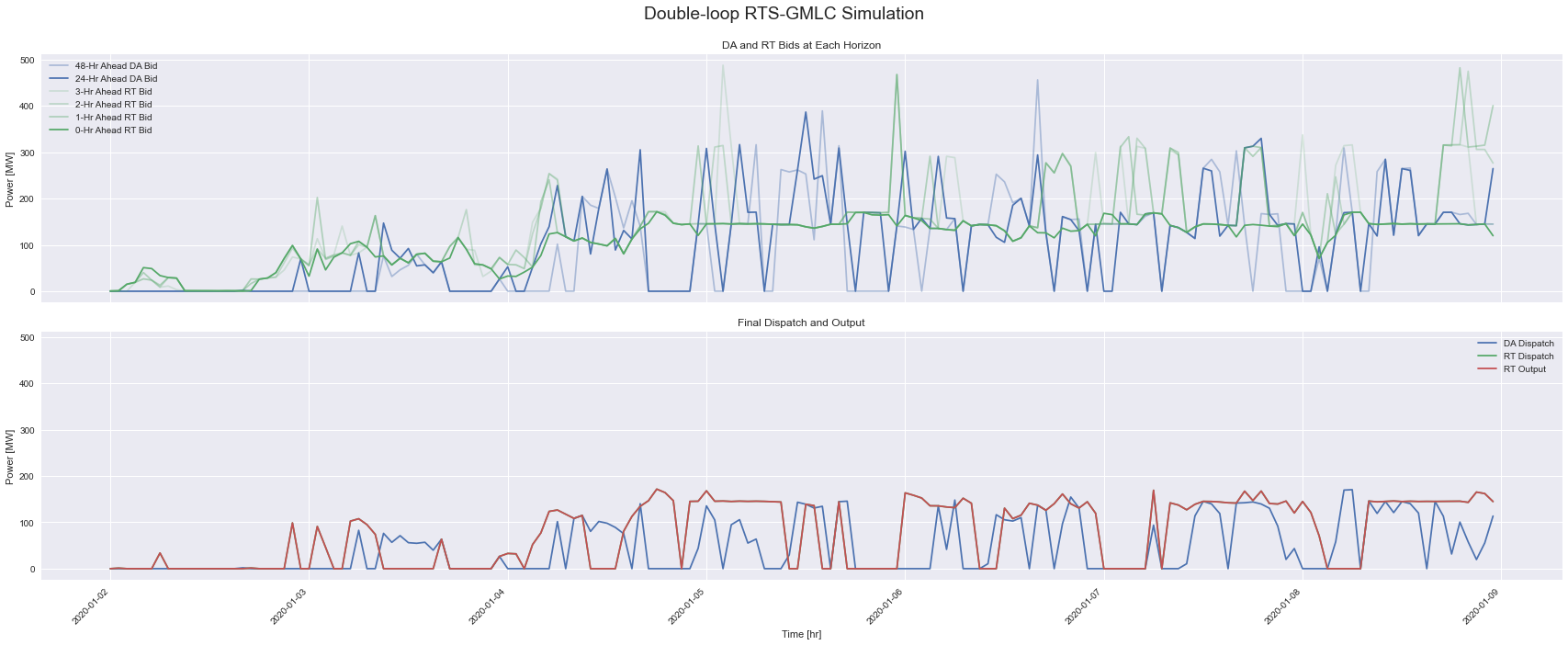

In contrast to the wind plant above which bids its DA resource forecast and its RT resource forecast at $0/MWh marginal cost, the Wind + Battery IES is shifting the times and prices to sell energy. The bidding process for both the DA and RT market take place across multiple horizons within the staggered, forward-rolling UC and ED problems. As the Bidder receives more information about its state within each time horizon, it updates its bids. This is shown in the first plot in the top row, where

the final DA and RT Bid are 24-Hr Ahead DA Bid and 0-Hr Ahead RT Bid. The second row shows the DA Dispatch and RT Dispatch from Prescient, and the delivered RT Output.

[12]:

fig, ax = plt.subplots(2, 1, figsize=(24, 10), sharex=True)

ax[0].plot(time_index, np.append([0] * 24, da_bidder_df[da_bidder_df['Horizon [hr]'] >= 24][da_bid_powers].sum(axis=1))[time_slice], color='b', alpha=0.4, label="48-Hr Ahead DA Bid")

ax[0].plot(time_index, da_bidder_df[da_bidder_df['Horizon [hr]'] < 24][da_bid_powers].sum(axis=1)[time_slice], color='b', alpha=1, label="24-Hr Ahead DA Bid")

ax[0].plot(time_index, np.append([0] * 3, rt_bidder_df[rt_bidder_df['Horizon [hr]'] == 3][rt_bid_powers].sum(axis=1))[time_slice], color='g', alpha=0.2, label="3-Hr Ahead RT Bid")

ax[0].plot(time_index, np.append([0] * 2, rt_bidder_df[rt_bidder_df['Horizon [hr]'] == 2][rt_bid_powers].sum(axis=1))[time_slice], color='g', alpha=0.3, label="2-Hr Ahead RT Bid")

ax[0].plot(time_index, np.append([0] * 1, rt_bidder_df[rt_bidder_df['Horizon [hr]'] == 1][rt_bid_powers].sum(axis=1))[time_slice], color='g', alpha=0.4, label="1-Hr Ahead RT Bid")

ax[0].plot(time_index, rt_bidder_df[rt_bidder_df['Horizon [hr]'] == 0]['RT Power 0 [MW]'].values[time_slice], color='g', alpha=1, label="0-Hr Ahead RT Bid")

ax[1].plot(time_index, prescient_df['Dispatch DA'].values[time_slice], color='b', label='DA Dispatch')

ax[1].plot(time_index, prescient_df['Dispatch'].values[time_slice], color='g', label='RT Dispatch')

ax[1].plot(time_index, tracker_df[tracker_df['Horizon [hr]'] == 0][['Power Output [MW]']], color='r', label='RT Output')

ax[1].set_ylim(ax[0].get_ylim())

format_plt(fig, ax, mod_ticks=False, titles=["DA and RT Bids at Each Horizon", "Final Dispatch and Output"], suptitle="Double-loop RTS-GMLC Simulation")

Analyzing the Wind + Battery IES Performance: Tracker and Settlement

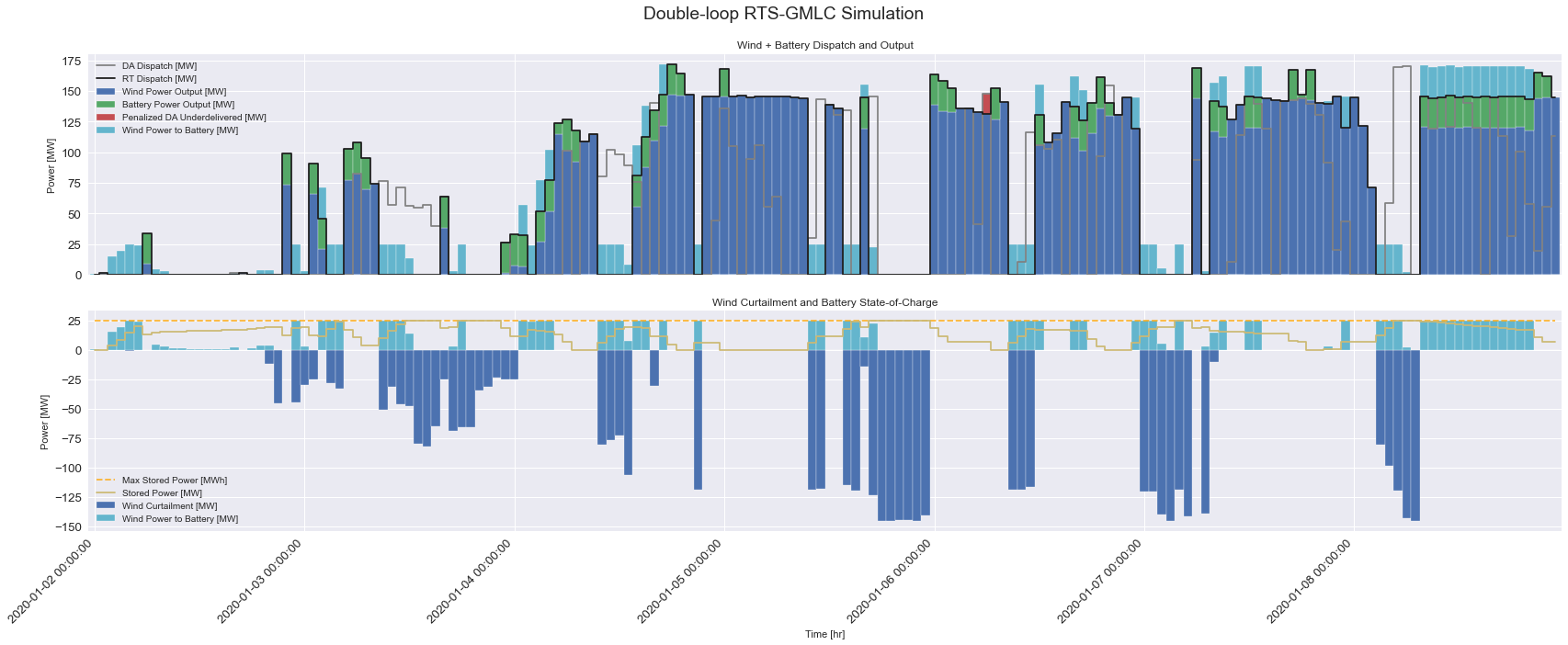

The first plot shows the double-loop simulation results. Max power has increased due to battery capacity. In comparison to the original result plotted above, there’s different DA Dispatch due to using RT forecast instead of DA forecast. Also, where there were a few times where the wind plant had negative revenue due to Penalized DA Underdelivered when the RT price was higher than the DA price, here, there is only one instance of being penalized for missing a DA promise. However, there

appears to be more curtailed energy, and the battery is full at least once a day, often more.

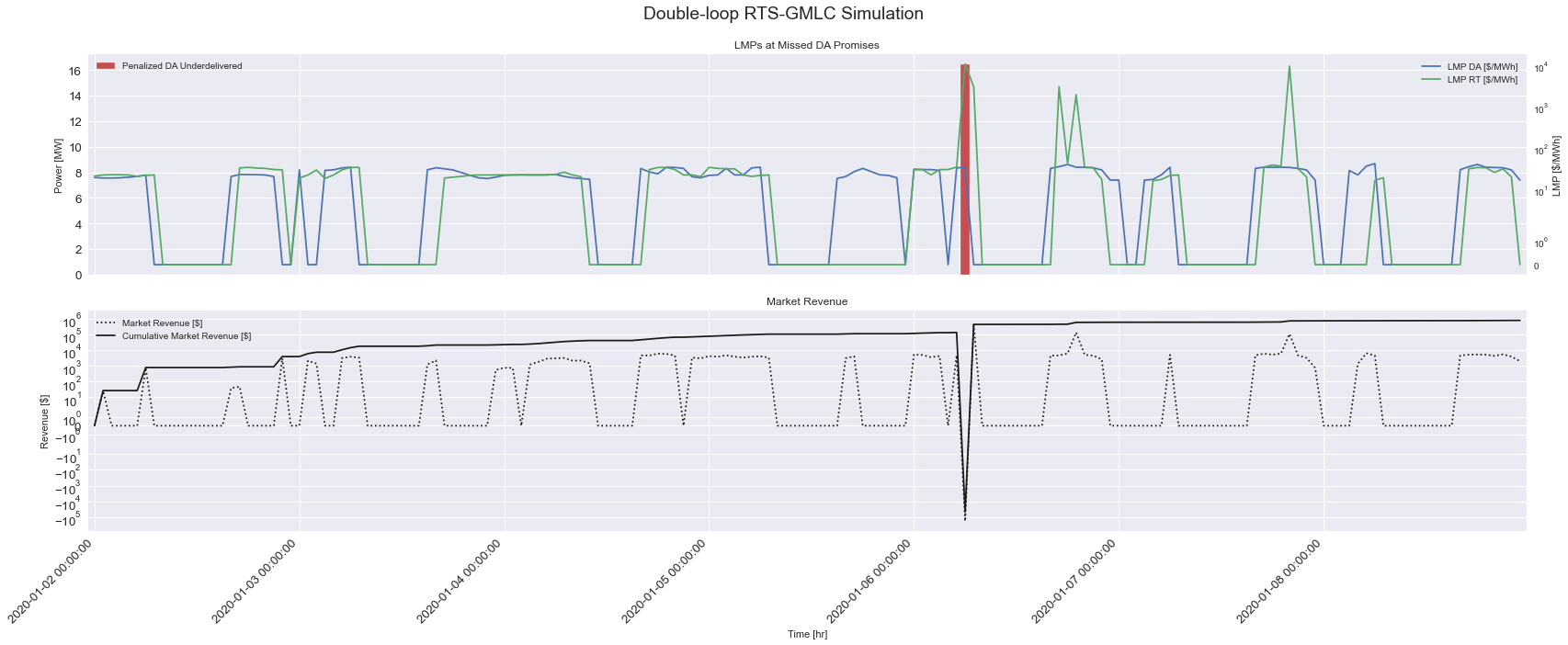

The second plot shows the impact on the Generator’s Unit Market Revenue.

[13]:

tracker_df.loc[:, 'Penalized DA Underdelivered'] = 0

prescient_df["Penalized DA Underdelivered"] = ((prescient_df['Dispatch DA'] - prescient_df['Dispatch']) * (prescient_df['LMP'] > prescient_df['LMP DA'])).clip(lower=0).values

tracker_df.loc[tracker_df['Horizon [hr]'] == 0, 'Penalized DA Underdelivered [MW]'] = prescient_df["Penalized DA Underdelivered"].values

fig, ax = plt.subplots(2, 1, figsize=(24, 10), sharex=True)

cols = ["Wind Power Output [MW]", "Battery Power Output [MW]", 'Penalized DA Underdelivered [MW]', "Wind Power to Battery [MW]"]

ax[0].plot(prescient_df['Dispatch DA'].values, drawstyle="steps-mid", label='DA Dispatch [MW]', color='grey')

ax[0].plot(tracker_df.loc[tracker_df['Horizon [hr]'] == 0]['Total Power Output [MW]'].values, drawstyle="steps-mid", label='RT Dispatch [MW]', color='k')

tracker_df.loc[tracker_df['Horizon [hr]'] == 0][cols].plot(kind='bar', width=1, stacked=True, ax=ax[0], color=['b', 'g', 'r', 'c'])

tracker_df.loc[tracker_df['Horizon [hr]'] == 0]['Wind Curtailment [MW]'].plot(kind='bar', width=1, stacked=True, ax=ax[1])

tracker_df.loc[tracker_df['Horizon [hr]'] == 0]["Wind Power to Battery [MW]"].plot(kind='bar', width=1, stacked=True, ax=ax[1], color='c')

ax[1].plot([battery_pmax] * len(time_index), linestyle="dashed", label='Max Stored Power [MWh]', alpha=0.8, color='orange')

ax[1].plot(tracker_df.loc[tracker_df['Horizon [hr]'] == 0]['State of Charge [MWh]'].values / 4, drawstyle="steps-mid", label='Stored Power [MW]', color='y')

format_plt(fig, ax, titles=["Wind + Battery Dispatch and Output", "Wind Curtailment and Battery State-of-Charge"], suptitle="Double-loop RTS-GMLC Simulation")

[14]:

fig, ax = plt.subplots(2, 1, figsize=(24, 10), sharex=True)

prescient_df["Penalized DA Underdelivered"].plot(ax=ax[0], color='r', kind='bar', width=1)

ax0 = ax[0].twinx()

ax0.set_yscale('symlog')

ax0.plot(prescient_df['LMP DA'].values, label="LMP DA [$/MWh]")

ax0.plot(prescient_df['LMP'].values, label='LMP RT [$/MWh]')

ax0.legend(loc='upper right')

ax0.set_ylabel("LMP [$/MWh]")

ax0.grid(None)

ax[1].set_yscale('symlog')

ax[1].plot(prescient_df['Unit Market Revenue'].values, color='k', linestyle=':', label="Market Revenue [$]")

ax[1].plot(prescient_df['Unit Market Revenue'].cumsum().values, color='k', label="Cumulative Market Revenue [$]")

format_plt(fig, ax, y_labels=['Power [MW]', 'Revenue [$]'], titles=["LMPs at Missed DA Promises", "Market Revenue"], suptitle="Double-loop RTS-GMLC Simulation")

ax[0].legend(loc='upper left')

[14]:

<matplotlib.legend.Legend at 0x7fd7ab1c6970>

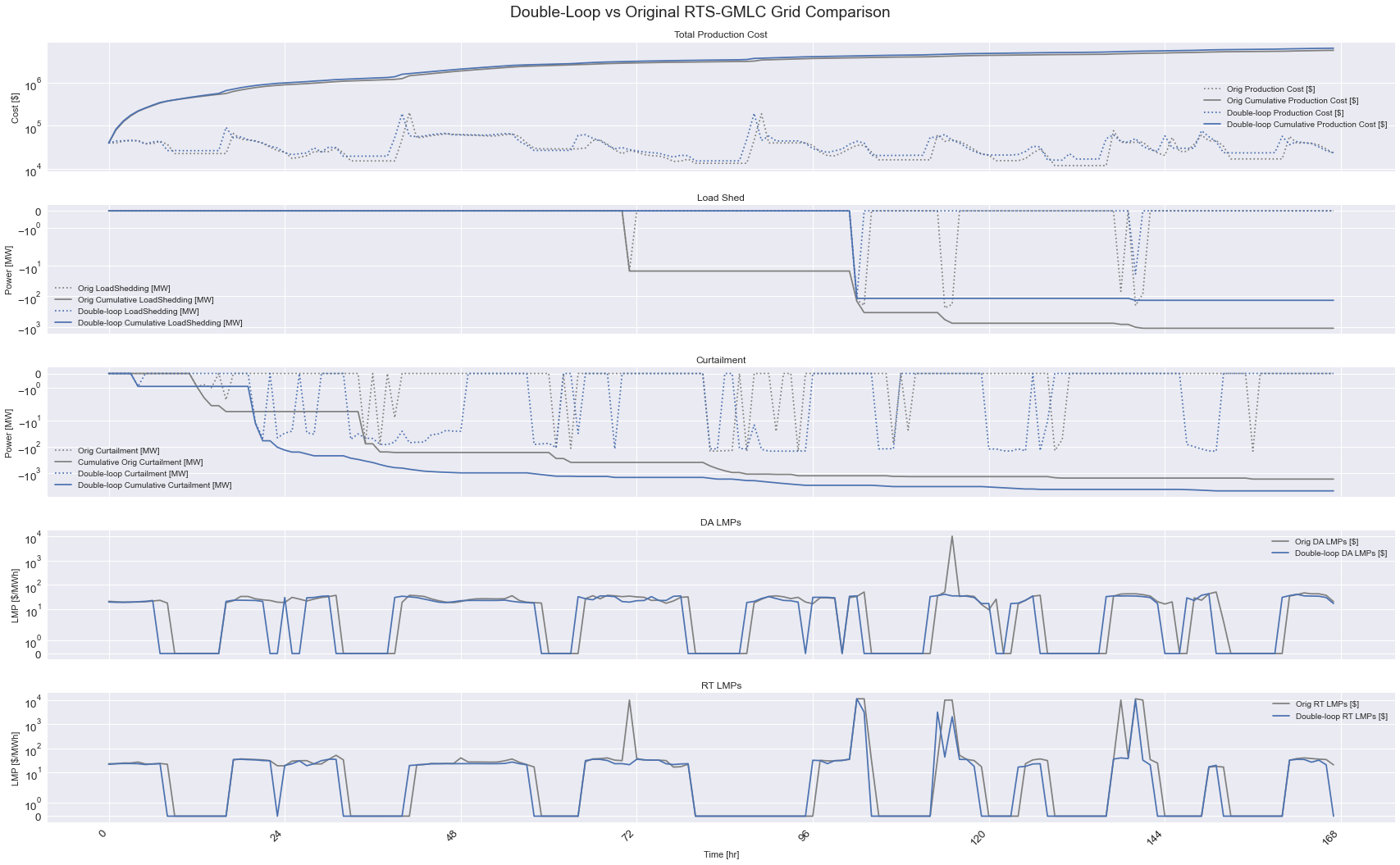

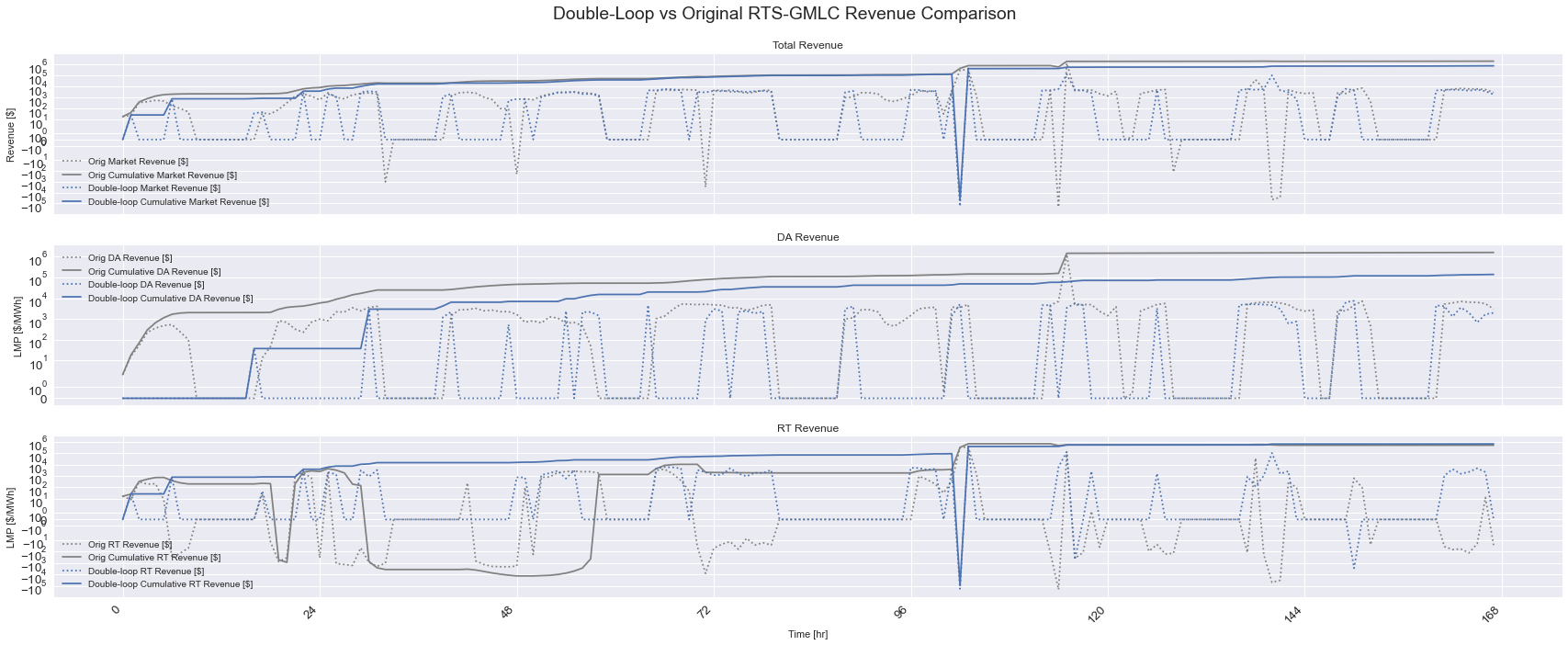

Analyzing the Wind + Battery IES Performance: Comparison to Original RTS-GMLC Simulation

The plots below show the changes in the electricity market which impact the plant’s economic performance and the grid’s production and reliability.

[15]:

fig, ax = plt.subplots(3, 1, figsize=(24, 10), sharex=True)

ax[0].set_yscale('symlog')

ax[0].plot(orig_outputs_df['Unit Market Revenue'].values, color='grey', linestyle=':', label="Orig Market Revenue [$]")

ax[0].plot(orig_outputs_df['Unit Market Revenue'].cumsum().values, color='grey', label="Orig Cumulative Market Revenue [$]")

ax[0].plot(prescient_df['Unit Market Revenue'].values, color='b', linestyle=':', label="Double-loop Market Revenue [$]")

ax[0].plot(prescient_df['Unit Market Revenue'].cumsum().values, color='b', label="Double-loop Cumulative Market Revenue [$]")

ax[1].set_yscale('symlog')

da_rev = orig_outputs_df['Output DA'] * orig_outputs_df['LMP DA']

ax[1].plot(da_rev.values, color='grey', linestyle=':', label="Orig DA Revenue [$]")

ax[1].plot(da_rev.cumsum().values, color='grey', label="Orig Cumulative DA Revenue [$]")

da_rev = prescient_df['Dispatch DA'] * prescient_df['LMP DA']

ax[1].plot(da_rev.values, color='b', linestyle=':', label="Double-loop DA Revenue [$]")

ax[1].plot(da_rev.cumsum().values, color='b', label="Double-loop Cumulative DA Revenue [$]")

ax[2].set_yscale('symlog')

rt_rev = (orig_outputs_df['Output'] - orig_outputs_df['Output DA']) * orig_outputs_df['LMP']

ax[2].plot(rt_rev.values, color='grey', linestyle=':', label="Orig RT Revenue [$]")

ax[2].plot(rt_rev.cumsum().values, color='grey', label="Orig Cumulative RT Revenue [$]")

rt_rev = (tracker_df[tracker_df['Horizon [hr]'] == 0]['Power Output [MW]'] - prescient_df['Dispatch DA']) * prescient_df['LMP']

ax[2].plot(rt_rev.values, color='b', linestyle=':', label="Double-loop RT Revenue [$]")

ax[2].plot(rt_rev.cumsum().values, color='b', label="Double-loop Cumulative RT Revenue [$]")

format_plt(fig, ax, y_labels=['Revenue [$]', "LMP [$/MWh]", "LMP [$/MWh]"], titles=["Total Revenue", 'DA Revenue', 'RT Revenue'], suptitle="Double-Loop vs Original RTS-GMLC Revenue Comparison")

[16]:

fig, ax = plt.subplots(5, 1, figsize=(24, 15), sharex=True)

ax[0].set_yscale('symlog')

ax[0].plot(orig_outputs_df['TotalCosts'].values, color='grey', linestyle=':', label="Orig Production Cost [$]")

ax[0].plot(orig_outputs_df['TotalCosts'].cumsum().values, color='grey', label="Orig Cumulative Production Cost [$]")

ax[0].plot(prescient_df['TotalCosts'].values, color='b', linestyle=':', label="Double-loop Production Cost [$]")

ax[0].plot(prescient_df['TotalCosts'].cumsum().values, color='b', label="Double-loop Cumulative Production Cost [$]")

ax[1].set_yscale('symlog')

ax[1].plot(orig_outputs_df['LoadShedding'].values * -1, color='grey', linestyle=':', label="Orig LoadShedding [MW]")

ax[1].plot(orig_outputs_df['LoadShedding'].cumsum().values * -1, color='grey', label="Orig Cumulative LoadShedding [MW]")

ax[1].plot(prescient_df['LoadShedding'].values * -1, color='b', linestyle=':', label="Double-loop LoadShedding [MW]")

ax[1].plot(prescient_df['LoadShedding'].cumsum().values * -1, color='b', label="Double-loop Cumulative LoadShedding [MW]")

ax[2].set_yscale('symlog')

ax[2].plot(orig_outputs_df['Curtailment'].values, color='grey', linestyle=':', label="Orig Curtailment [MW]")

ax[2].plot(orig_outputs_df['Curtailment'].cumsum().values, color='grey', label="Cumulative Orig Curtailment [MW]")

ax[2].plot(tracker_df[tracker_df['Horizon [hr]'] == 0]['Wind Curtailment [MW]'].values, color='b', linestyle=':', label="Double-loop Curtailment [MW]")

ax[2].plot(tracker_df[tracker_df['Horizon [hr]'] == 0]['Wind Curtailment [MW]'].cumsum().values, color='b', label="Double-loop Cumulative Curtailment [MW]")

ax[3].set_yscale('symlog')

ax[3].plot(orig_outputs_df['LMP DA'].values, color='grey', label="Orig DA LMPs [$]")

ax[3].plot(prescient_df['LMP DA'].values, color='b', label="Double-loop DA LMPs [$]")

ax[4].set_yscale('symlog')

ax[4].plot(orig_outputs_df['LMP'].values, color='grey', label="Orig RT LMPs [$]")

ax[4].plot(prescient_df['LMP'].values, color='b', label="Double-loop RT LMPs [$]")

format_plt(fig, ax, y_labels=['Cost [$]', "Power [MW]", "Power [MW]", "LMP [$/MWh]", "LMP [$/MWh]"], titles=["Total Production Cost", 'Load Shed', 'Curtailment', 'DA LMPs', 'RT LMPs'], suptitle="Double-Loop vs Original RTS-GMLC Grid Comparison")